3 Types of Risk in Insurance:- Insurance is a crucial aspect of financial planning, and understanding the different types of risks associated with it is essential. Insurance risk refers to the uncertainty regarding potential loss and is the reason why people pay premiums on their insurance policies. There are three types of risks in insurance: financial and non-financial risks, pure and speculative risks, and fundamental and particular risks. These risks can be measured in monetary terms, and understanding them is critical for effective financial planning and risk management.

3 Types of Risk in Insurance

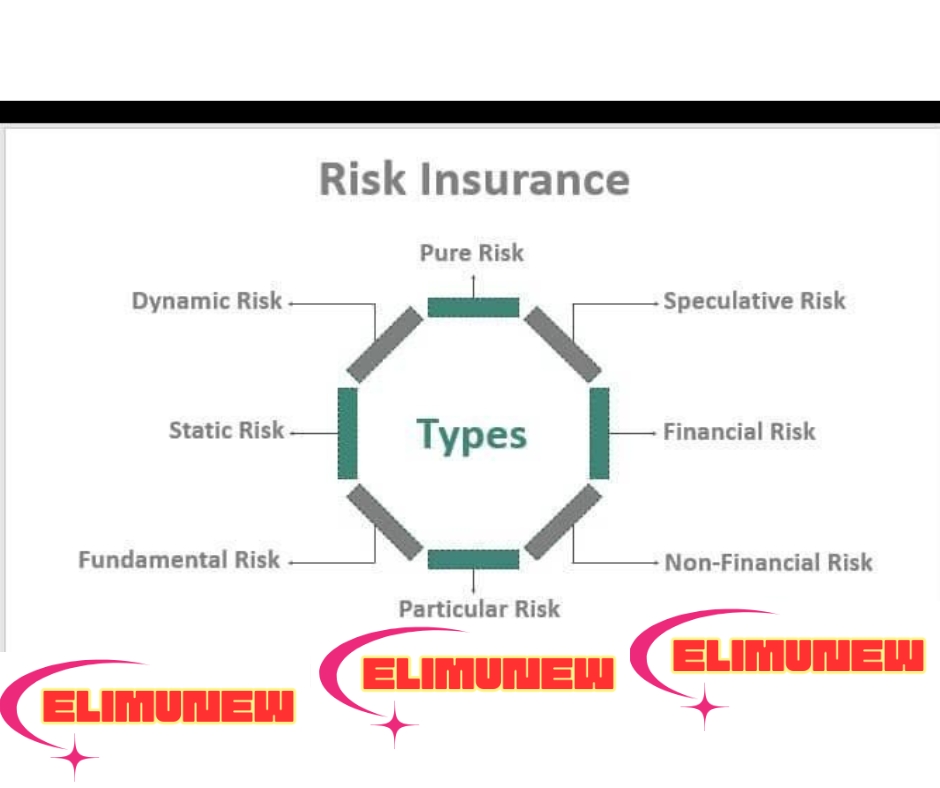

Financial risks are those that can be measured in terms of monetary value. They include risks such as theft, loss, property damage, or someone being injured. Non-financial risks, on the other hand, cannot be measured in monetary terms. They include risks such as reputational damage, legal liabilities, or regulatory risks. Pure risks are those that result in a loss only, or at best, a break-even situation. Speculative risks, on the other hand, involve the possibility of gain as well as loss. Fundamental risks are those that mostly emanate from nature, such as natural disasters, while particular risks are those that are specific to a particular industry or business.

Understanding the different types of risks in insurance is essential for effective risk management and choosing the right financial services. It also has a significant impact on insurance premiums and regulatory considerations. By assessing and managing risk effectively, individuals and businesses can mitigate the impact of potential losses and ensure better financial stability.

Key Takeaways

- There are three types of risks in insurance: financial and non-financial risks, pure and speculative risks, and fundamental and particular risks.

- Understanding these risks is critical for effective financial planning, risk management, and choosing the right financial services.

- Proper assessment and management of risk can help mitigate the impact of potential losses and ensure better financial stability.

Understanding Risk in Insurance

In insurance, risk refers to the likelihood of an insured event occurring and the subsequent financial impact it may have on the insurer. Insurers assess risks based on various factors, such as the insured individual’s age, health, occupation, lifestyle, and the nature of the insured item or property.

There are three types of risks in insurance: financial and non-financial risks, pure and speculative risks, and fundamental and particular risks. Financial risks can be measured in monetary terms and are related to the financial health of the insured individual or entity. Non-financial risks, on the other hand, cannot be measured in monetary terms and are related to factors such as reputation, legal liability, and operational risks.

Pure risks are a loss only or, at best, a break-even situation, meaning there is no possibility of a gain. Speculative risks, on the other hand, offer the possibility of gain or loss. Fundamental risks are the risks mostly emanating from nature, such as natural disasters, while particular risks are specific to an individual or entity, such as theft or damage to property.

Insurance companies use various tools and techniques to manage risks, such as risk transfer, risk avoidance, risk retention, and risk reduction. Risk transfer involves transferring the risk to another party, such as an insurance company. Risk avoidance involves avoiding activities that are considered risky, while risk retention involves accepting the risk and self-insuring against it. Risk reduction involves taking measures to reduce the likelihood of a risk occurring, such as installing fire alarms or using safer equipment.

Understanding the types of risks in insurance is important for effective financial planning, risk management, and choosing the right financial services. By understanding the risks involved, individuals and entities can make informed decisions about the types of insurance coverage they need and the level of risk they are willing to accept.

Also See: Marine Insurance Warranties: What You Need to Know

Types of Risk in Insurance

Insurance is a mechanism to transfer risk from the insured to the insurer. It is important for the insurer to understand the types of risk involved in insurance to provide the best possible coverage to the insured. There are three types of risks in insurance: pure risk, speculative risk, and operational risk.

Pure Risk

Pure risk is a type of risk that has only two possible outcomes, either a loss or no loss. The loss can be financial or physical, but it cannot result in a gain. For example, the risk of a car accident is a pure risk because it can result in a financial loss, but it cannot result in a gain. Insurance companies typically cover pure risks because they are insurable.

You Might Like: Rate Making in Marine Insurance: A Comprehensive Guide

Speculative Risk

Speculative risk is a type of risk that has three possible outcomes: a gain, a loss, or no change. For example, investing in the stock market is a speculative risk because it can result in a gain, a loss, or no change. Insurance companies do not typically cover speculative risks because they are not insurable.

Operational Risk

Operational risk is a type of risk that arises from the day-to-day operations of a business. It can be caused by human error, system failures, or external events. For example, a cyber attack on a company’s computer system is an operational risk. Insurance companies offer coverage for operational risks through various types of insurance policies such as cyber insurance, professional liability insurance, and errors and omissions insurance.

Understanding the types of risks involved in insurance is crucial for both the insurer and the insured. It helps the insurer determine the premiums to be charged and the coverage to be provided, and it helps the insured choose the right insurance policy to mitigate the risks they face.

Assessment and Management of Risk

Assessment and management of risk are essential components of the insurance industry. Insurers must evaluate the risks associated with offering coverage to policyholders and manage those risks to ensure their financial stability. There are several steps involved in the assessment and management of risk in insurance.

Risk Assessment

Risk assessment involves identifying, analyzing, and evaluating the risks associated with insuring a particular policyholder or group of policyholders. Insurers use a variety of techniques to assess risk, including data analysis, statistical modeling, and expert judgment. The goal of risk assessment is to determine the likelihood and potential severity of a loss, which helps insurers set appropriate premiums and offer appropriate coverage.

Risk Management

Once insurers have assessed the risks associated with insuring a particular policyholder or group of policyholders, they must manage those risks to ensure their financial stability. Risk management involves identifying, assessing, and prioritizing risks, and then taking steps to mitigate or eliminate those risks. Insurers use a variety of techniques to manage risk, including risk avoidance, risk reduction, risk transfer, and risk retention.

Importance of Effective Risk Management

Effective risk management is essential for insurers to remain financially stable and profitable. Insurers must be able to accurately assess and manage risks to ensure they are offering appropriate coverage and setting fair premiums. Failure to effectively manage risk can result in financial losses for insurers, which can ultimately lead to insolvency. Therefore, insurers must continuously evaluate and improve their risk management processes to ensure their long-term success in the industry.

Mitigation Strategies for Insurance Risks

When it comes to insurance, risk mitigation strategies are essential to protecting both the insurer and the insured. Insurance companies use a variety of methods to mitigate risk, including:

1. Risk Assessment

The first step in risk mitigation is to assess the risks involved. Insurance professionals and experts meticulously analyze various factors that could pose threats, ranging from natural disasters to economic downturns. This thorough assessment forms the foundation for developing effective mitigation strategies.

2. Control the Risk

An action plan is created to reduce the severity or probability of a risk occurring. Using this strategy, the risk is identified and accepted, and then a corrective procedure is implemented to reduce or remove its impact.

3. Transfer the Risk

Sometimes, risks are mitigated through transference. Insurance is a tool that lets you transfer the financial risk of certain types of losses to your carrier. As you consider risk management strategies, you can assess which types of insurance policies might make sense for your business given the risks you face. For example, liability policies can help you hedge against legal risk. Property policies can help you protect your investment in your physical assets.

It is important to note that risk mitigation is not a one-time event. It is an ongoing process that requires constant monitoring, evaluation, and adjustment as new risks emerge. By implementing effective risk mitigation strategies, insurance companies can minimize their exposure to risk and ensure that they are able to meet their obligations to policyholders.

The Impact of Risk on Insurance Premiums

Insurance companies use risk assessment to determine the likelihood and potential financial impact of various risks, allowing them to set appropriate premium rates, coverage, and deductibles. The higher the risk, the more likely the insurer will have to pay out a claim. As a result, the higher the premium will be.

There are several factors that insurance companies consider when assessing risk. These include the type of coverage, the deductible amount, the policyholder’s age, gender, and health status, and the likelihood of a claim being filed. For example, a policyholder who is older, has a history of health problems, or is involved in a high-risk occupation may pay a higher premium than someone who is younger, healthy, and has a low-risk job.

Another factor that can impact insurance premiums is the level of risk associated with the insured asset or activity. For example, a car that is more likely to be stolen or involved in an accident will have a higher premium than a car that is less likely to be stolen or involved in an accident. Similarly, a home located in an area prone to natural disasters, such as floods or earthquakes, will have a higher premium than a home located in a low-risk area.

Finally, insurance companies may also consider the policyholder’s personal risk factors, such as credit history, criminal record, or previous insurance claims. A policyholder with a poor credit score or a history of insurance claims may be viewed as a higher risk and may pay a higher premium.

In summary, the impact of risk on insurance premiums is significant. Insurance companies assess risk based on a variety of factors, including the type of coverage, the insured asset or activity, and the policyholder’s personal risk factors. The higher the risk, the higher the premium will be.

Regulatory Considerations in Risk Management

In the insurance industry, regulatory compliance is a critical aspect of risk management. Insurance companies must comply with various regulations that are designed to protect consumers and ensure the stability of the financial system. Failure to comply with these regulations can result in significant penalties and reputational damage. Therefore, insurance companies must have a robust risk management framework in place to ensure compliance with these regulations.

One of the most important regulatory considerations in risk management is the Solvency II Directive. Solvency II is a set of regulations that aim to strengthen the solvency of insurance companies operating in the European Union. The directive requires insurance companies to maintain sufficient capital to cover their risks, and to implement a risk management framework that is commensurate with their risk profile. This includes the identification, assessment, and management of all risks that may have a material impact on the company’s financial position.

Another important regulatory consideration is the National Association of Insurance Commissioners (NAIC) Own Risk and Solvency Assessment (ORSA). ORSA is a regulatory framework that requires insurance companies to conduct a self-assessment of their risk management practices. This includes the identification of all material risks, the assessment of their potential impact, and the implementation of appropriate risk mitigation strategies. ORSA is a critical tool for insurance companies to ensure that they have a robust risk management framework in place, and that they are complying with all relevant regulations.

Finally, insurance companies must also comply with various anti-money laundering (AML) and counter-terrorism financing (CTF) regulations. AML and CTF regulations are designed to prevent the use of the financial system for illicit purposes, such as money laundering or terrorist financing. Insurance companies must have appropriate policies, procedures, and controls in place to identify and report suspicious activity, and to ensure that they are not inadvertently facilitating criminal activity.

In summary, regulatory compliance is a critical aspect of risk management in the insurance industry. Insurance companies must comply with various regulations, including Solvency II, ORSA, and AML/CTF regulations. Failure to comply with these regulations can result in significant penalties and reputational damage. Therefore, insurance companies must have a robust risk management framework in place to ensure compliance with these regulations.

Frequently Asked Questions

What are the three main types of risk covered by insurance?

The three main types of risk covered by insurance are pure risks, speculative risks, and operational risks. Pure risks are risks that have only two possible outcomes: loss or no loss. Speculative risks, on the other hand, are risks where there is a possibility of gain or loss. Operational risks are risks that arise from the day-to-day operations of a business.

How do insurance companies classify risks?

Insurance companies classify risks by assessing the likelihood and severity of potential losses. Factors such as age, health, lifestyle, occupation, and location are taken into consideration when determining risk classes and premium pricing. Insurance companies also use statistical data and actuarial tables to calculate risks.

What are examples of the different types of insurance risk?

Examples of pure risks include car accidents, natural disasters, and theft. Speculative risks include gambling and investing in the stock market. Operational risks include employee errors, equipment breakdowns, and cyber attacks.

What is the difference between subjective and objective risk in insurance?

Subjective risk is the perceived level of risk by an individual or organization, while objective risk is the actual level of risk based on statistical data and analysis. Insurance companies use objective risk to determine premium pricing, while subjective risk can influence an individual’s decision to purchase insurance.

How do fundamental risks differ from particular risks in insurance?

Fundamental risks are risks that affect the entire economy or large groups of people, such as natural disasters or war. Particular risks are risks that affect only a specific individual or group, such as illness or a car accident. Insurance companies typically cover particular risks, while fundamental risks are often covered by government programs.

What role does risk management play in the insurance industry?

Risk management plays a crucial role in the insurance industry by helping insurance companies identify and assess potential risks and develop strategies to mitigate those risks. This includes implementing policies and procedures to reduce the likelihood of losses, as well as developing contingency plans in the event of a loss. Effective risk management can help insurance companies maintain financial stability and provide better coverage to their policyholders.

3 thoughts on “3 Types of Risk in Insurance: Understanding the Basics”