Insurance: Definitions and Features Explained:- Insurance is a concept that has been around for centuries, and it has evolved significantly over time. Insurance is a form of risk management that allows individuals and businesses to protect themselves from financial losses. Insurance policies are contracts between an individual or entity and an insurance company, where the company agrees to provide financial protection or reimbursement for losses in exchange for premiums paid by the policyholder.

Insurance: Definitions and Features Explained

Understanding the fundamentals of insurance is essential to be able to make informed decisions about what type of insurance coverage is needed. Insurance policies can vary greatly in terms of coverage, premiums, and deductibles. It is crucial to understand the policy structure, types of insurance, and insurance providers to make the best decisions for your unique situation. Additionally, insurance regulation and risk management play a significant role in the insurance industry, and it is important to stay up to date on trends and innovations in the field.

Key Takeaways

- Insurance is a form of risk management that allows individuals and businesses to protect themselves from financial losses.

- It is essential to understand the policy structure, types of insurance, and insurance providers to make informed decisions about insurance coverage.

- Staying up to date on insurance regulation, risk management, and industry trends is crucial for making informed decisions about insurance.

Insurance Fundamentals

Definition of Insurance

Insurance is a legal contract between an individual or entity (the policyholder) and an insurance company. The policyholder pays a premium to the insurance company in exchange for financial protection or reimbursement against losses resulting from covered events. The insurance company pools the premiums from many policyholders to pay out claims to those who experience losses.

You Might Like: 16 Types of Fire Insurance Policies: A Comprehensive Guide

Purpose of Insurance

The purpose of insurance is to protect individuals, businesses, and other entities from financial loss due to unexpected events. Insurance provides peace of mind by transferring the risk of loss from the policyholder to the insurance company. By purchasing insurance, individuals can protect themselves and their assets from unexpected events such as accidents, illnesses, and natural disasters.

Principles of Insurance

There are several principles of insurance that guide the insurance industry. These principles include:

- Utmost Good Faith: Both the policyholder and the insurance company must act in good faith and provide accurate information to each other.

- Indemnity: The insurance company must compensate the policyholder for the actual amount of loss suffered, up to the limits of the policy.

- Contribution: If the policyholder has multiple insurance policies covering the same loss, each insurer will contribute to the loss in proportion to the amount of coverage provided.

- Subrogation: After paying a claim, the insurance company may take legal action to recover the amount paid from any third party responsible for the loss.

- Proximate Cause: The insurance company will only pay for losses that are caused by covered events listed in the policy.

- Mitigation: The policyholder must take reasonable steps to prevent further loss after an event covered by the policy has occurred.

Types of Insurance

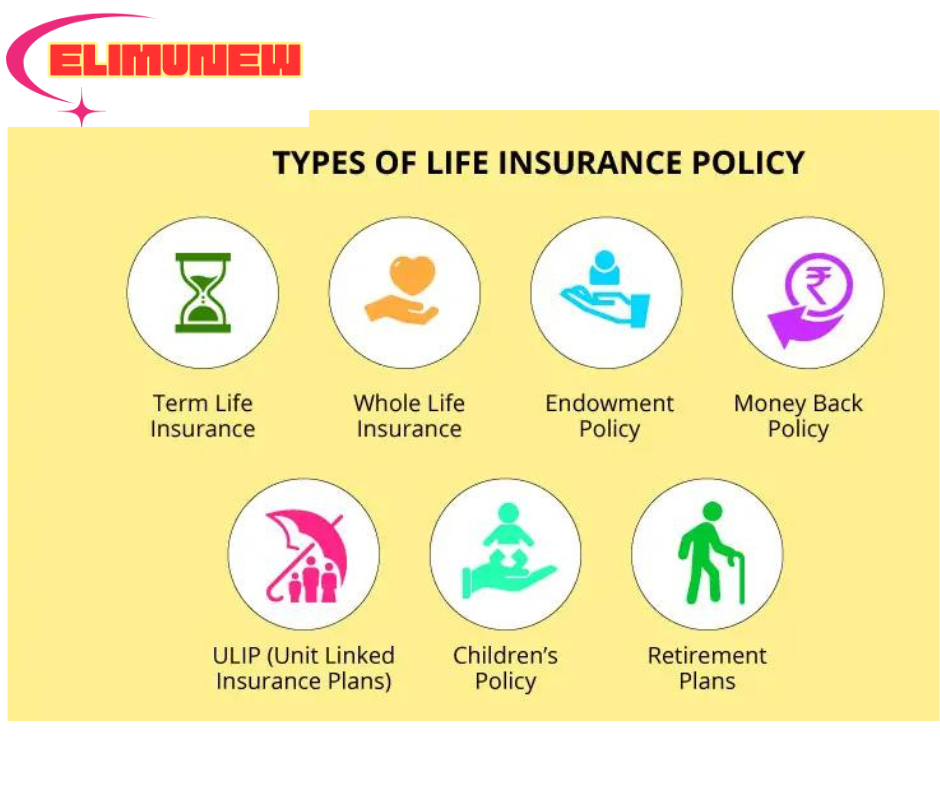

Life Insurance

Life insurance is a type of insurance that pays out a sum of money upon the death of the insured person. This can provide financial support to the beneficiaries of the policyholder, such as family members or business partners. There are two main types of life insurance: term life insurance and permanent life insurance. Term life insurance provides coverage for a specified period of time, while permanent life insurance provides coverage for the lifetime of the insured person.

Health Insurance

Health insurance is a type of insurance that covers the cost of medical expenses incurred by the insured person. This can include expenses related to hospitalization, surgery, prescription drugs, and other medical procedures. Health insurance can be provided by an employer or purchased by an individual. There are several types of health insurance plans, including health maintenance organizations (HMOs), preferred provider organizations (PPOs), and point of service (POS) plans.

Property and Casualty Insurance

Property and casualty insurance is a type of insurance that provides coverage for damage to property and liability for injuries or damage caused by the insured person. Property insurance covers damage to buildings and other structures, as well as personal property such as furniture and clothing. Casualty insurance covers liability for injuries or damage caused by the insured person, such as in an automobile accident or a slip and fall accident.

Liability Insurance

Liability insurance is a type of insurance that provides coverage for legal claims made against the insured person. This can include claims related to bodily injury, property damage, or personal injury. Liability insurance can be purchased by individuals or businesses, and is often required by law for certain activities such as driving a car or operating a business. There are several types of liability insurance, including general liability insurance, professional liability insurance, and product liability insurance.

Policy Structure

Insurance policies are legal contracts that outline the terms and conditions of coverage between the insured and the insurer. Policies can be complex, but understanding their structure can help policyholders make informed decisions about their coverage. Here are some common features of insurance policies:

Insurance Premiums

The insurance premium is the amount the policyholder pays to the insurer for coverage. Premiums can be paid monthly, quarterly, or annually, and can vary depending on the type of policy, the coverage limits, and the policyholder’s risk factors. Premiums can also be affected by the policyholder’s claims history and credit score.

Policy Limits

Policy limits are the maximum amount an insurer will pay out for a covered loss. Policyholders should carefully review their policy limits to ensure they have adequate coverage in case of a loss. If the cost of a loss exceeds the policy limit, the policyholder may be responsible for paying the difference.

Deductibles

A deductible is the amount the policyholder must pay out of pocket before the insurer will pay for a covered loss. Deductibles can vary depending on the type of policy and the coverage limits. Higher deductibles can lower the insurance premium, but can also increase the policyholder’s out-of-pocket expenses in the event of a loss.

Coverage Exclusions

Insurance policies also contain coverage exclusions, which are situations or events that are not covered by the policy. It is important for policyholders to review their policy exclusions carefully to understand what is and is not covered. For example, a homeowner’s insurance policy may exclude coverage for damage caused by floods or earthquakes.

Overall, understanding the structure of an insurance policy can help policyholders make informed decisions about their coverage and ensure they have adequate protection in the event of a loss.

Insurance Providers

Insurance providers are entities that offer insurance policies to individuals and organizations. These providers can be private companies or government-run programs.

Private Insurers

Private insurance companies are for-profit entities that offer a variety of insurance policies to individuals and businesses. These policies can include health insurance, life insurance, auto insurance, and more. Private insurers set their own rates and coverage options, and customers can choose the policy that best fits their needs.

Private insurers are regulated by state and federal laws to ensure that they operate fairly and provide adequate coverage to their customers. These regulations also require insurers to maintain a certain level of financial stability to ensure that they can meet their obligations to policyholders.

Government Insurance Programs

Government insurance programs are run by federal or state governments and are designed to provide insurance coverage to individuals who may not be able to obtain coverage through private insurers. These programs can include Medicare, Medicaid, and the Children’s Health Insurance Program (CHIP).

Medicare is a federal program that provides health insurance to individuals over the age of 65, as well as to some younger individuals with disabilities. Medicaid is a joint federal-state program that provides health insurance to low-income individuals and families. CHIP provides health insurance to children from low-income families who are not eligible for Medicaid.

Government insurance programs are funded by taxes and are subject to strict regulations to ensure that they operate efficiently and provide adequate coverage to their beneficiaries.

Overall, insurance providers play a critical role in protecting individuals and organizations from financial losses due to unforeseen events. Whether through private insurers or government-run programs, individuals and businesses have access to a variety of insurance options to meet their needs.

Insurance Regulation

Insurance regulation is the government’s oversight of the insurance market to ensure fairness and professionalism among those working for the insurance industry, to prevent the market from collapsing, and to democratize insurance. There are several regulatory bodies responsible for overseeing the insurance industry.

Regulatory Bodies

In the United States, insurance regulation is primarily the responsibility of state governments. Each state has its own insurance department, which is responsible for overseeing insurance companies that operate within its borders. These departments are responsible for licensing insurance companies, monitoring their financial solvency, and enforcing state insurance laws and regulations.

In addition to state insurance departments, there are also several national organizations that play a role in insurance regulation. The National Association of Insurance Commissioners (NAIC) is a voluntary association of state insurance commissioners that develops model laws and guidelines for state insurance regulation. The Federal Insurance Office (FIO) is a federal agency that monitors the insurance industry and provides advice to the federal government on insurance matters.

Consumer Protections

Insurance regulation is designed to protect consumers from unfair or deceptive practices by insurance companies. State insurance departments have the authority to investigate complaints from consumers and take action against insurance companies that engage in unfair or deceptive practices. In addition, many states have enacted consumer protection laws that provide additional protections to insurance consumers.

Compliance and Enforcement

Insurance companies are required to comply with state insurance laws and regulations. State insurance departments have the authority to investigate insurance companies that are suspected of violating state insurance laws and regulations. If an insurance company is found to be in violation, the state insurance department may take enforcement action, which can include fines, license revocation, or other penalties.

In conclusion, insurance regulation is an essential part of the insurance industry. It protects consumers from unfair or deceptive practices and ensures that insurance companies operate in a fair and professional manner. Regulatory bodies, consumer protections, and compliance and enforcement are all important components of insurance regulation.

Risk Management

Risk management is an essential aspect of insurance that involves identifying, assessing, and mitigating risks that may lead to financial loss. Insurance companies use various risk management strategies to minimize the impact of risks on their financial stability. This section will discuss the different aspects of risk management in insurance.

Risk Assessment

Risk assessment involves identifying potential risks that may affect an individual or a business and evaluating their likelihood and potential impact. Insurance companies use various tools and techniques to assess risk, such as statistical analysis and actuarial science. By understanding the nature and extent of risks, insurance companies can determine the appropriate premiums to charge for insurance policies.

Risk Mitigation Strategies

Risk mitigation strategies involve taking steps to reduce the likelihood and impact of potential risks. Insurance companies use various risk mitigation strategies, such as diversification, asset allocation, and hedging. Diversification involves spreading investments across different asset classes to minimize the impact of market fluctuations. Asset allocation involves investing in assets that have a low correlation with each other to reduce overall portfolio risk. Hedging involves using financial instruments to offset potential losses.

The Role of Reinsurance

Reinsurance is a risk management strategy that involves transferring some of the risks that an insurance company assumes to another insurance company. Reinsurance helps insurance companies manage their exposure to risks and ensure that they have sufficient capital to pay claims. Reinsurance can be either proportional or non-proportional. Proportional reinsurance involves sharing risks and premiums between the primary insurer and the reinsurer based on a predetermined percentage. Non-proportional reinsurance involves transferring risks and premiums to the reinsurer only when losses exceed a certain threshold.

In conclusion, risk management is an essential aspect of insurance that involves identifying, assessing, and mitigating risks that may lead to financial loss. Insurance companies use various risk management strategies to minimize the impact of risks on their financial stability, such as risk assessment, risk mitigation, and reinsurance. By understanding the nature and extent of risks, insurance companies can determine the appropriate premiums to charge for insurance policies.

Claims Process

When it comes to insurance, the claims process is the most important aspect of the coverage. This is where the insurer and the insured come together to resolve an issue. The claims process typically consists of three main stages: filing a claim, claim investigation, and settlement and payout.

Filing a Claim

The first step in the claims process is to file a claim. The insured must notify the insurance company of any loss or damage that has occurred. The claim should include all relevant information, such as the policy number, the date and time of the incident, and a detailed description of the loss or damage.

Claim Investigation

Once the claim has been filed, the insurance company will investigate the claim. This may involve an inspection of the property, interviews with witnesses, or a review of medical records. The purpose of the investigation is to determine the cause and extent of the loss or damage, and to verify that the claim is covered under the policy.

Settlement and Payout

After the investigation is complete, the insurance company will make a decision on the claim. If the claim is approved, the insurer will offer a settlement amount to the insured. The amount of the settlement will be based on the terms of the policy, the extent of the loss or damage, and any applicable deductibles. Once the insured accepts the settlement offer, the insurer will issue a payout to cover the cost of the loss or damage.

In conclusion, the claims process is a critical component of insurance coverage. It is important for the insured to understand the steps involved in filing a claim, the investigation process, and the settlement and payout process. By being knowledgeable about the claims process, the insured can ensure that they receive the coverage they need in the event of a loss or damage.

Insurance Trends and Innovations

Technological Advancements

The insurance industry is undergoing significant changes, many of which are fueled by technological advancements. According to McKinsey, a handful of accelerating technology trends are poised to transform the very nature of insurance. For instance, in auto insurance, risk will shift from drivers to the artificial intelligence (AI) and software behind self-driving cars. Satellites, drones, and real-time data sets will give insurers unprecedented visibility into the risk around facilities. These technologies will help insurers to price risk more accurately and provide better coverage to their customers.

Emerging Insurance Products

The insurance industry is also experiencing a proliferation of new products and services. According to Deloitte, there has been a surge in the number of insurtech startups that are developing innovative insurance products and services. These products and services are designed to meet the needs of the modern consumer, who is looking for more personalized and flexible insurance solutions.

Market Dynamics

The insurance market is also being shaped by changing market dynamics. For instance, according to KPMG, embedded insurance could exceed $70 billion in premiums by 2030. A survey conducted by Chubb Insurance showed that 81% of financial executives who make decisions about insurance products think embedded insurance will transform from a “nice-to-have” into a “must-have.” This trend is likely to continue as more companies look to embed insurance into their products and services.

In conclusion, the insurance industry is undergoing significant changes, driven by technological advancements, emerging insurance products, and changing market dynamics. These changes are likely to continue, and insurance companies that can adapt to these changes will be well-positioned to succeed in the future.

Frequently Asked Questions

What constitutes the definitions section of an insurance policy?

The definitions section of an insurance policy outlines the key terms used throughout the policy. This section is important because it helps policyholders understand the meaning of important terms and phrases used in the policy. For example, the definitions section may include the meaning of terms such as “insured,” “policyholder,” “premium,” and “deductible.”

Can you explain the five fundamental principles of insurance?

The five fundamental principles of insurance are: (1) Utmost good faith, (2) Insurable interest, (3) Indemnity, (4) Contribution, and (5) Subrogation. These principles are designed to ensure that insurance policies are fair and equitable for both the insurer and the policyholder.

What are the seven principles that underpin the insurance industry?

The seven principles that underpin the insurance industry are: (1) Insurable interest, (2) Utmost good faith, (3) Indemnity, (4) Contribution, (5) Subrogation, (6) Loss minimization, and (7) Causa proxima. These principles are designed to ensure that insurance policies are fair and equitable for both the insurer and the policyholder.

How do the features of insurance policies benefit policyholders?

The features of insurance policies benefit policyholders by providing financial protection against unforeseen events. For example, insurance policies can provide coverage for property damage, medical expenses, and liability claims. Additionally, insurance policies can provide peace of mind by reducing the financial risk associated with certain activities.

What are the various types of insurance available to consumers?

There are many different types of insurance available to consumers, including: (1) Auto insurance, (2) Homeowners insurance, (3) Life insurance, (4) Health insurance, (5) Disability insurance, and (6) Long-term care insurance. Each type of insurance provides coverage for specific risks and events.

What roles do insurance companies play beyond underwriting and risk management?

Insurance companies play a variety of roles beyond underwriting and risk management. For example, insurance companies may offer policyholders access to resources such as legal advice, financial planning, and risk assessment tools. Additionally, insurance companies may provide support to policyholders in the event of a claim, such as by coordinating repairs or providing emergency assistance.

3 thoughts on “Insurance: Definitions and Features Explained”