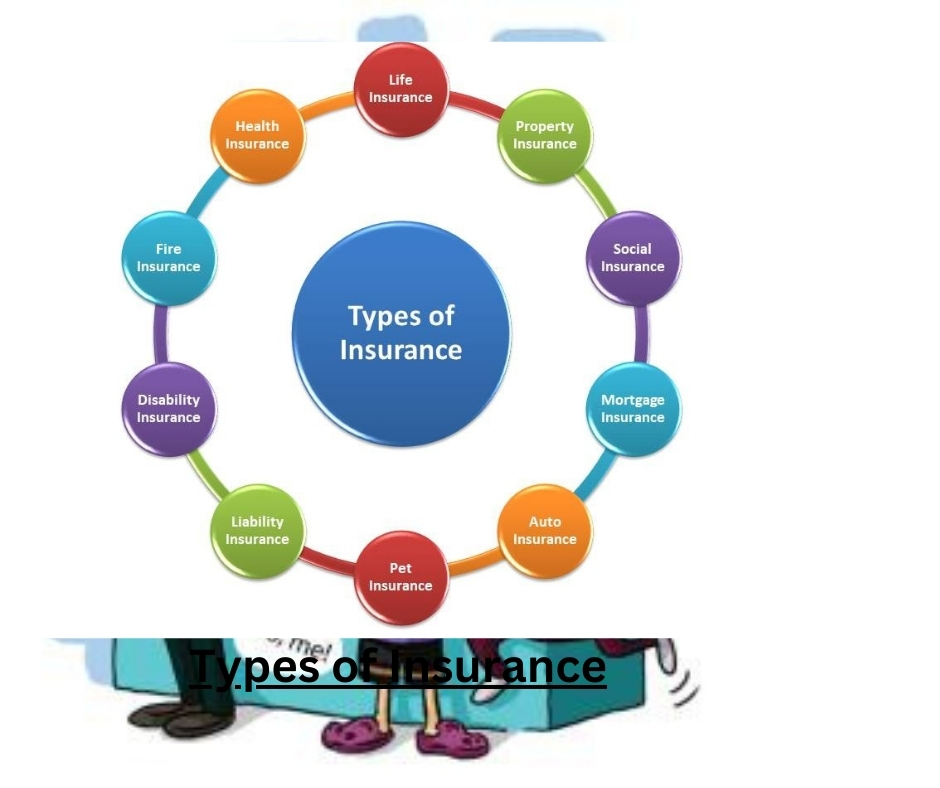

Types of Insurance;- Insurance is a means of protection against financial loss. It is a form of risk management, primarily used to hedge against the risk of a contingent or uncertain loss. Insurance is a contract between the insurer and the insured, known as the policyholder, which determines the claims that the insurer is legally required to pay. In exchange for an initial payment, known as the premium, the insurer promises to pay for loss caused by perils covered under the policy language.

Types of Insurance

There are many types of insurance policies available, each designed to meet the specific needs of individuals, businesses, and other organizations. Understanding the different types of insurance policies available is essential for making informed decisions about which policy is right for you. In this article, we will provide a comprehensive guide to insurance types, including personal insurance types, property and casualty insurance, commercial insurance types, specialty insurance products, and government-provided insurance.

Key Takeaways

- Insurance is a form of risk management that protects against financial loss.

- There are many types of insurance policies available to meet the specific needs of individuals, businesses, and other organizations.

- Understanding the different types of insurance policies available is essential for making informed decisions about which policy is right for you.

Understanding Insurance Fundamentals

Insurance is a contract between an individual or entity and an insurance company that provides financial protection or reimbursement against losses. The individual or entity pays a premium to the insurance company, and in exchange, the insurance company agrees to cover the losses specified in the policy.

There are various types of insurance policies available, including auto, home, life, health, and liability insurance. Each type of insurance policy covers different types of losses. For example, auto insurance covers losses related to car accidents, while home insurance covers losses related to damage to the home or personal property.

Insurance policies have several components, including the premium, deductible, and coverage limits. The premium is the amount paid by the individual or entity to the insurance company for coverage. The deductible is the amount that the individual or entity must pay out of pocket before the insurance company begins to cover the losses. The coverage limit is the maximum amount that the insurance company will pay for losses covered under the policy.

It is important to understand the terms and conditions of an insurance policy before purchasing it. Individuals or entities should carefully review the policy to ensure that it covers the types of losses they are concerned about and that the coverage limits are adequate. Additionally, individuals or entities should compare policies from different insurance companies to find the best coverage at the most affordable price.

Personal Insurance Types

Personal insurance policies are designed to provide coverage for individuals and their families. There are various types of personal insurance policies available, each tailored to safeguard different aspects of your life and property. Here are the four main types of personal insurance:

Also See: Life Insurance Assignment and Nomination: Understanding the Basics

Health Insurance

Health insurance is the most important type of insurance an individual can buy. It provides coverage for medical expenses, including doctor visits, hospital stays, and prescription drugs. Health insurance policies can be purchased individually or through an employer. The coverage and cost of the policy depend on the individual’s health, age, and lifestyle.

Life Insurance

Life insurance provides financial protection for an individual’s loved ones in the event of their death. It is designed to provide a lump sum payment to the beneficiaries named in the policy. There are two main types of life insurance: term life insurance and permanent life insurance. Term life insurance provides coverage for a specified period of time, while permanent life insurance provides coverage for the entire life of the insured.

Disability Insurance

Disability insurance provides income replacement in the event an individual becomes disabled and is unable to work. There are two types of disability insurance: short-term disability insurance and long-term disability insurance. Short-term disability insurance provides coverage for a few weeks or months, while long-term disability insurance provides coverage for an extended period of time.

Long-Term Care Insurance

Long-term care insurance provides coverage for the cost of long-term care, such as nursing home care, home health care, and assisted living facilities. It is designed to provide financial protection for individuals who require long-term care services due to a chronic illness or disability. Long-term care insurance policies vary in coverage and cost, depending on the individual’s age and health status.

Overall, personal insurance policies are essential for protecting an individual’s health, income, and assets. It is important to understand the different types of personal insurance policies available and choose the ones that best fit your needs and budget.

See Also: National Insurance: Everything You Need to Know

Property and Casualty Insurance

Property and casualty (P&C) insurance is a type of insurance that provides coverage for property and liability risks. P&C insurance policies are designed to protect individuals and businesses from financial losses due to damage to property and liability for causing injury or damage to others.

Homeowners Insurance

Homeowners insurance is a type of P&C insurance that provides coverage for damage to a person’s home and personal property. This type of insurance also provides liability coverage in case someone is injured on the homeowner’s property. Homeowners insurance policies typically cover damage caused by fire, theft, vandalism, and natural disasters.

Auto Insurance

Auto insurance is another type of P&C insurance that provides coverage for damage to a person’s vehicle and liability for causing injury or damage to others while driving. Auto insurance policies typically cover damage caused by accidents, theft, vandalism, and natural disasters.

Renters Insurance

Renters insurance is a type of P&C insurance that provides coverage for a person’s personal property in a rented dwelling. This type of insurance also provides liability coverage in case someone is injured while on the renter’s property. Renters insurance policies typically cover damage caused by fire, theft, vandalism, and natural disasters.

Natural Disaster Insurance

Natural disaster insurance is a type of P&C insurance that provides coverage for damage caused by natural disasters such as floods, earthquakes, hurricanes, and tornadoes. This type of insurance is typically not included in standard homeowners or renters insurance policies and must be purchased separately.

Overall, P&C insurance is an essential component of the insurance industry, designed to protect individuals and businesses from financial losses due to damage to property and liability for causing injury or damage to others.

Commercial Insurance Types

Commercial insurance is a type of insurance policy that covers businesses against losses and damages caused by events such as natural disasters, theft, and liability claims. There are several types of commercial insurance policies, each designed to protect businesses against specific risks.

General Liability Insurance

General liability insurance is a type of commercial insurance that covers businesses against claims of bodily injury, property damage, and personal injury. This type of insurance is essential for businesses that interact with the public, such as retail stores, restaurants, and service providers.

Professional Liability Insurance

Professional liability insurance, also known as errors and omissions insurance, is a type of commercial insurance that protects businesses against claims of negligence, errors, and omissions in the provision of professional services. This type of insurance is essential for businesses that provide professional services, such as accountants, lawyers, and consultants.

Product Liability Insurance

Product liability insurance is a type of commercial insurance that covers businesses against claims of injury or damage caused by their products. This type of insurance is essential for businesses that manufacture, distribute, or sell products.

Commercial Property Insurance

Commercial property insurance is a type of commercial insurance that covers businesses against losses and damages to their physical assets, such as buildings, equipment, and inventory. This type of insurance is essential for businesses that own or lease property.

Overall, commercial insurance is an essential investment for businesses of all sizes and industries. By choosing the right type of commercial insurance policy, businesses can protect themselves against the risks and uncertainties of the modern business world.

Specialty Insurance Products

Specialty insurance policies provide coverage for unique situations, events, or assets that require specialized attention. These policies are tailored to address specific risks that may not be adequately covered by general insurance policies. Here are some of the most common types of specialty insurance products:

Travel Insurance

Travel insurance provides protection for unexpected events that may occur while traveling, such as trip cancellations, medical emergencies, or lost luggage. This type of insurance can give travelers peace of mind knowing that they will be covered in case of unforeseen circumstances.

Pet Insurance

Pet insurance covers the cost of veterinary care for pets in case of illness or injury. This type of insurance can be especially helpful for pet owners who want to ensure that their furry companions receive the best possible care without having to worry about the cost.

Event Insurance

Event insurance provides coverage for events such as weddings, concerts, and other special occasions. This type of insurance can protect event organizers from financial losses in case of cancellation, postponement, or other unforeseen circumstances.

Cyber Insurance

Cyber insurance provides protection against cyber threats such as data breaches, cyber attacks, and other online risks. This type of insurance can be especially beneficial for businesses that rely on technology to operate and store sensitive information.

Specialty insurance products can provide valuable protection for unique situations and assets. It is important to carefully consider the risks associated with your specific situation and choose a policy that provides adequate coverage.

Government-Provided Insurance

Government-provided insurance refers to insurance programs that are funded and administered by the government. These programs are designed to provide financial support and assistance to individuals who may not be able to afford private insurance or who may not have access to it.

Social Security Benefits

Social Security is a federal program that provides financial benefits to retired workers, their spouses, and their children. It also provides benefits to individuals who are disabled or have lost a spouse or parent who was eligible for Social Security benefits. The program is funded through payroll taxes, which are paid by workers and their employers.

Medicare and Medicaid

Medicare is a federal health insurance program that provides coverage to individuals who are 65 or older, as well as to individuals who have certain disabilities or medical conditions. The program is funded through payroll taxes and premiums paid by beneficiaries. Medicaid, on the other hand, is a joint federal and state program that provides health insurance to individuals with low incomes. The program is funded by both the federal government and the states.

Unemployment Insurance

Unemployment insurance is a joint federal and state program that provides financial assistance to individuals who have lost their jobs through no fault of their own. The program is funded through payroll taxes paid by employers. To be eligible for unemployment insurance, individuals must have worked a certain number of hours and earned a minimum amount of wages during a designated period of time.

Overall, government-provided insurance programs play an important role in providing financial support and assistance to individuals who may not be able to afford private insurance or who may not have access to it. These programs are funded through a combination of payroll taxes, premiums, and government funds, and they provide a safety net for individuals during times of need.

Insurance Policy Components

When it comes to insurance, there are a few key components that make up the policy. Understanding these components can help you make informed decisions about the type of insurance you need and the coverage limits that are right for you.

Premiums

The premium is the amount of money you pay to the insurance company in exchange for coverage. It can be paid monthly, quarterly, or annually. The amount you pay will depend on a variety of factors, including the type of insurance you need, your age, your health, and the coverage limits you choose.

Deductibles

The deductible is the amount of money you pay out of pocket before the insurance company begins to pay for covered expenses. For example, if you have a $1,000 deductible on your auto insurance policy and you get into an accident that causes $5,000 in damage, you would pay the first $1,000 and the insurance company would cover the remaining $4,000.

Coverage Limits

The coverage limit is the maximum amount the insurance company will pay for covered expenses. For example, if you have a $100,000 coverage limit on your homeowners insurance policy and your house is destroyed in a fire, the insurance company will pay up to $100,000 to repair or replace your home.

Exclusions

Exclusions are specific situations or events that are not covered by the insurance policy. It’s important to read your policy carefully to understand what is and is not covered. For example, most homeowners insurance policies do not cover damage caused by floods or earthquakes, so you may need to purchase separate coverage for those events.

Understanding these key components of insurance policies can help you make informed decisions about the coverage you need and the limits that are right for you.

Risk Management and Insurance

Risk management and insurance are essential for individuals and businesses alike. Insurance provides financial protection against unexpected events that can result in significant financial losses. Risk management is the process of identifying, assessing, and managing risks to minimize the likelihood and impact of losses.

There are many types of insurance available, including life, health, auto, home, and business insurance. Each type of insurance is designed to protect against specific risks. For example, life insurance provides financial support to loved ones in the event of the policyholder’s death, while auto insurance protects against damages resulting from car accidents.

Effective risk management involves identifying potential risks and taking steps to mitigate them. This can include implementing safety measures, such as installing smoke detectors or fire suppression systems, or developing emergency response plans. Insurance is an important component of risk management because it provides financial protection in the event that these measures fail or are insufficient.

When selecting insurance policies, it’s important to consider the risks that are most relevant to your situation. For example, if you own a home, you’ll want to ensure that you have adequate homeowner’s insurance to protect against damage from natural disasters, theft, or other unforeseen events. Similarly, if you own a business, you’ll want to consider liability insurance to protect against lawsuits and other legal claims.

Overall, risk management and insurance are critical components of financial planning. By identifying potential risks and taking steps to mitigate them, individuals and businesses can protect themselves against financial losses and ensure their long-term financial stability.

Choosing the Right Insurance Policy

Choosing the right insurance policy can be a daunting task, but it is crucial to ensure that you have adequate coverage in case of unexpected events. Here are some tips to help you choose the right insurance policy:

1. Assess Your Needs

Before you start looking for an insurance policy, you need to assess your needs and determine what you want to protect. For example, if you own a car, you may want to consider purchasing auto insurance. If you have a family, you may want to consider life insurance. Assessing your needs will help you narrow down your options and choose the right insurance policy.

2. Compare Policies

Once you have assessed your needs, you should compare policies from different insurance companies to find the best coverage at the best price. You should compare the coverage, deductibles, premiums, and any exclusions or limitations of each policy. This will help you make an informed decision and choose the policy that best meets your needs and budget.

3. Consider the Reputation of the Insurance Company

When choosing an insurance policy, it is important to consider the reputation of the insurance company. You want to choose a company that has a good track record of paying claims and providing excellent customer service. You can research the reputation of an insurance company by checking online reviews and ratings.

4. Seek Professional Advice

If you are unsure about which insurance policy to choose, you should seek professional advice. You can consult with an insurance agent or broker who can help you navigate the complex world of insurance and find the right policy for your needs. A professional can also help you understand the terms and conditions of the policy and answer any questions you may have.

By following these tips, you can choose the right insurance policy that provides adequate coverage and meets your needs and budget.

Frequently Asked Questions

What does comprehensive car insurance cover?

Comprehensive car insurance typically covers damages to your car that are not caused by a collision, such as theft, vandalism, fire, and natural disasters. It may also cover damages caused by hitting an animal or falling objects. However, it’s important to note that specific coverage can vary depending on the insurance company and the policy.

How does comprehensive insurance differ from collision insurance?

Comprehensive insurance covers damages to your car that are not caused by a collision, while collision insurance covers damages caused by a collision with another vehicle or object. Essentially, comprehensive insurance covers non-collision damages, while collision insurance covers collision damages.

What are the essential types of insurance everyone should have?

The most essential types of insurance that everyone should have include auto insurance, home or renters insurance, health insurance, and life insurance. These policies can provide financial protection in case of unexpected events, such as accidents, illnesses, or death.

Can you explain the different types of car insurance and what they cover?

The different types of car insurance include liability insurance, collision insurance, comprehensive insurance, personal injury protection (PIP) insurance, and uninsured/underinsured motorist insurance. Liability insurance is required by law in most states and covers damages to others in an accident that you are responsible for. Collision insurance covers damages to your own car in an accident, while comprehensive insurance covers non-collision damages. PIP insurance covers medical expenses for you and your passengers in an accident, while uninsured/underinsured motorist insurance covers damages caused by a driver without insurance or with insufficient insurance.

What is the difference between full coverage and comprehensive insurance?

Full coverage typically refers to having both comprehensive and collision insurance, as well as liability insurance. Comprehensive insurance covers non-collision damages, while collision insurance covers collision damages. Therefore, comprehensive insurance is a part of full coverage, but full coverage also includes collision insurance and liability insurance.

What should be considered when choosing comprehensive health insurance?

When choosing comprehensive health insurance, it’s important to consider factors such as the cost of premiums, deductibles, and copayments, as well as the coverage provided for medical services and prescription drugs. It’s also important to consider whether the policy includes coverage for pre-existing conditions, and whether the policy is compatible with any existing health savings accounts or flexible spending accounts.

2 thoughts on “Types of Insurance: A Comprehensive Guide to Insurance Types”